Balancing Mission and Math: The WeDevelopment FCU Analysis

A compelling community mission cannot override the mathematical reality of business model sustainability. Read the financial analysis of WeDevelopment FCU's recent NCUA conservatorship.

In the Living System methodology, a credit union is a biological entity requiring a continuous intake of metabolic energy—specifically, revenue and capital—to survive. A compelling community mission is vital, but it cannot override the mathematical reality of business model sustainability.

Governance boards possess a primary, non-negotiable responsibility: to protect the asset. When mission-driven initiatives are deployed without strict guardrails, appropriate pricing, and adequate capital buffers, the institution risks technical insolvency. A credit union cannot fulfill its cooperative purpose if it ceases to exist.

I recently had NotebookLM, a feature of Google's Gemini tool, conduct a financial trend analysis of WeDevelopment Federal Credit Union (WDFCU), an institution chartered in 2022 and placed into NCUA conservatorship in July 2026. We used call report data and our CU HealthScore model as the construct for the analysis. The resulting output clearly illustrates the tension between a noble community mission and the absolute requirements of financial safety.

I have included the analysis below in its entirety.

Tom Glatt

WeDevelopment Federal Credit Union: Financial Trend and Mission Analysis

Executive Summary

This trend analysis evaluates the financial performance and regulatory conservatorship of WeDevelopment Federal Credit Union (WDFCU) in Kansas City, Missouri. Chartered in July 2022 to serve the underserved community east of Troost Avenue, WDFCU was placed into conservatorship by the National Credit Union Administration (NCUA) on July 10, 2026.

WDFCU's financial metrics show that its credit score-independent lending model provided access to community capital but resulted in rising loan delinquency. This credit risk, combined with a high operating cost structure relative to its asset size, depleted the institution's capital reserves. The net worth ratio declined from a peak of 31.03% in Q1 2023 to -7.29% by Q1 2026, resulting in technical insolvency and subsequent conservatorship.

1. Credit Quality and Underwriting Standards

WDFCU aimed to transition residents from payday loans to credit union accounts. It offered 'Neighborhood Impact Loans' for minor home repairs up to $5,000 regardless of credit score, accepting scores as low as 550. WDFCU also offered signature and personal loans.

This underwriting model led to elevated credit risk:

- Delinquency Trends: The delinquency ratio rose from 0.00% in Q2 2023 to 4.54% in Q3 2023. The ratio was 7.18% in Q1 2024 and 12.79% in Q4 2024, before reaching a peak of 25.02% in Q4 2025. This meant 25.02% of the total loan portfolio was delinquent.

- Net Charge-Offs: Delinquent loans eventually resulted in credit losses. Net charge-offs rose to 18.65% of average loans in Q2 2024. A second increase occurred in Q1 2026, with net charge-offs reaching 27.66% of average loans. These losses reduced the credit union's net worth.

2. Deposit Funding and Member Balances

The credit union relied on local deposits to fund community loans. However, deposit trends showed high volatility and concentration:

- Average Deposit per Member: In Q1 2023, the average deposit per member was $22,094.86, reflecting initial institutional funding. This average declined by 86.3% to $3,015.76 by Q1 2026.

- Membership Growth: WDFCU increased its membership to 933 members by Q1 2026. The growth in members did not bring a proportional increase in total deposits, resulting in a lower average share balance per member.

3. Operating Expenses and Asset Scale

WDFCU operated on a high fixed-cost model, offering financial literacy and wealth coaching. Its assets totaled $2.63 million at the time of conservatorship.

- Operating Expense to Asset Ratio: WDFCU's operating expense to average assets ratio averaged 19.8% annually, with a peak of 23.56% in Q3 2024. By comparison, the credit union industry average operating expense ratio was 4.97% in Q1 2026.

- Return on Average Assets (ROAA): WDFCU recorded negative earnings in each operating quarter. Its ROAA averaged -19.1% over its lifespan and reached -36.79% in Q1 2026. This ongoing deficit depleted the credit union's initial equity capital.

4. Key Financial Turning Points in the Decline

| Phase / Date | HS | Risk Tier | Net Worth % | Delinquency % | Net Charge-Off % | ROAA % | Key Analytical Driver & Mission Link |

Q1 2023 (3/31/2023) | 5.353 | Tier 1 | 31.03% | 0.00% | 0.00% | -21.56% | Operational Commencement: WDFCU began full operations. Initial capital maintained a high Net Worth ratio, while operating costs generated an immediate deficit. |

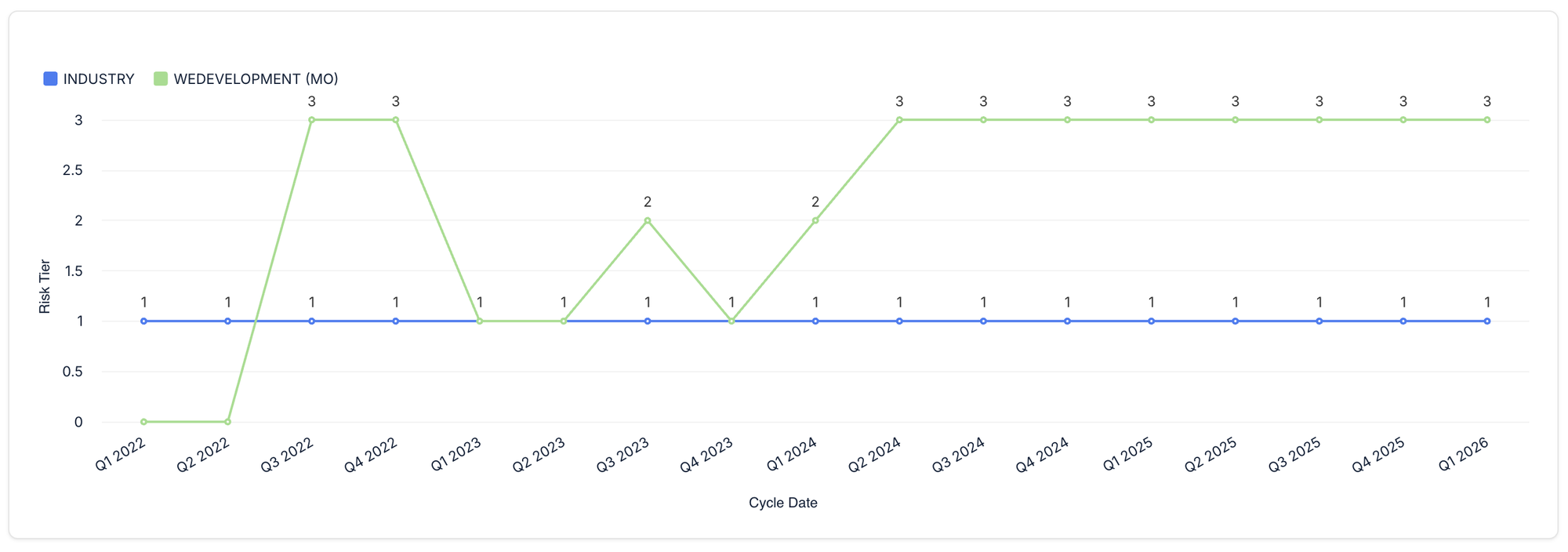

Q3 2023 (9/30/2023) | 4.618 | Tier 2 | 25.96% | 4.54% | 0.00% | -12.42% | Turning Point 1: WDFCU's delinquency ratio rose to 4.54% as initial community loans entered non-performance. |

Q2 2024 (6/30/2024) | 3.500 | Tier 3 | 11.71% | 4.51% | 18.65% | -25.88% | Turning Point 2: Charge-offs rose to 18.65% of average loans, reducing Net Worth from 19.13% to 11.71%. |

Q2 2025 (6/30/2025) | 3.176 | Tier 3 | 4.41% | 19.36% | 3.30% | -20.86% | Turning Point 3: Net Worth fell to 4.41%, which is below the 7% regulatory well-capitalized threshold. This triggered the Glatt Critical Override, placing WDFCU in Risk Tier 3. |

Q1 2026 (3/31/2026) | 1.706 | Tier 3 | -7.29% | 15.24% | 27.66% | -36.79% | Turning Point 4: Net charge-offs reached 27.66%, resulting in a negative net worth of -7.29% and a solvency ratio of 93.19%. The NCUA placed the institution into conservatorship in July 2026. |

5. Conclusion

WDFCU's financial trajectory illustrates the tension between a community-focused mission and the requirements of financial sustainability.

The organizers established the institution to provide a financial alternative to predatory lenders east of Troost. However, long-term viability requires balancing social goals with financial safety limits:

- Underwriting and Risk Mitigation: Approving home repair loans regardless of credit score without risk mitigants—such as risk-based pricing or specific capital reserves—resulted in credit risk that exceeded the credit union's capacity.

- Operating Scale: WDFCU's asset base of $2.63 million was insufficient to support a high-cost operating model that averaged 19.8% operating expenses to average assets. Without a larger deposit base to fund interest-earning assets, the credit union could not generate sufficient revenue to cover its expenses.

WDFCU was placed into conservatorship following technical insolvency. While member deposits remain insured up to $250,000, the financial history of WDFCU indicates that to serve communities of modest means, credit unions must maintain both financial safety and operational vitality.

Disclaimer: This analysis is based on WeDevelopment FCU historical Call Report data and the Glatt Consulting Group CU HealthScore model methodology.